When calculating the unadjusted basis immediately after acquisition (UBIA) in regards to the QBI deduction, what assets are included?

8995-A Instructions explain what assets are to be included in the calculation:

"For purposes of determining your UBIA for all qualified property, the unadjusted basis immediately after acquisition means the basis on the placed-in-service date. Qualified property includes tangible property subject to depreciation under section 167 that is held, and used in the production of QBI, by the trade or business (or aggregated trades or businesses) during and at the close of the tax year, for which the depreciable period hasn’t ended before the close of the tax year. The depreciable period ends on the later of 10 years after the property is first placed in service by you or the last day of the last full year in the applicable recovery period under section 168(c). Additional first-year depreciation under section 168 doesn’t affect the applicable recovery period.

Improvements to property that has already been placed in service are treated as separate qualified property..."

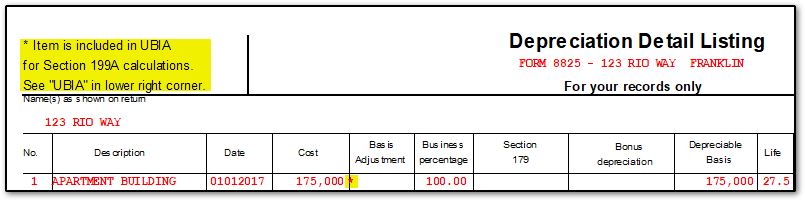

If assets are entered on the 4562 detail screens, the program will automatically calculate UBIA (see below if screens 6-9 are used instead*). The depreciation detail listing, FED DEPR Schedule, denotes the included assets with an asterisk to the right of the cost.

Then, the UBIA total for all assets is shown at the bottom right of the FED DEPR Schedule:

In a 1065 or 1120-S, this amount is carried to Wks QBI and then to the K-1 Wks QBI, based on ownership/shareholder percentage. Use the 199A screen to adjust the amount.

*If depreciation is being calculated outside the software and screens 6-9 are used to report depreciation, the software does not have enough information about the basis of each asset or the detail on the date acquired, life, etc. needed to automatically calculate what amount is UBIA. Therefore, when assets are not entered on the 4562 detail screens, you must enter the amount manually. Review the field help (F1) for additional details about this adjustment. The amount entered on the K screen, line X does not increase the amount that is shown on the FED DEPR Schedule (if any), but it does adjust the amount allocated to each shareholder/partner on their K-1 Wks QBI.

See the IRS Section 199A FAQs and 8995-A Instructions for more information.

On a scale of 1-5, please rate the helpfulness of this article

Optionally provide private feedback to help us improve this article...

Thank you for your feedback!