How do I elect to use the simplified method for my client’s office in home deduction in Drake Tax?

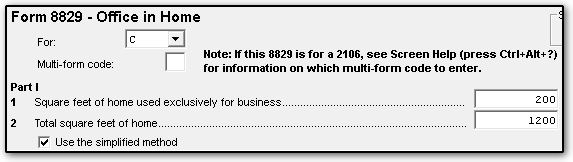

Taxpayers may elect to use a simplified method (instead of actual expenses) when figuring the deduction for business use of their home. To elect the simplified method, open the 8829 screen and select the applicable form or schedule in the For drop list. Enter a Multi-Form code, if applicable. Then enter the square footage of office on line 1, the total square footage of the home on line 2, and select the checkbox Use the simplified method:

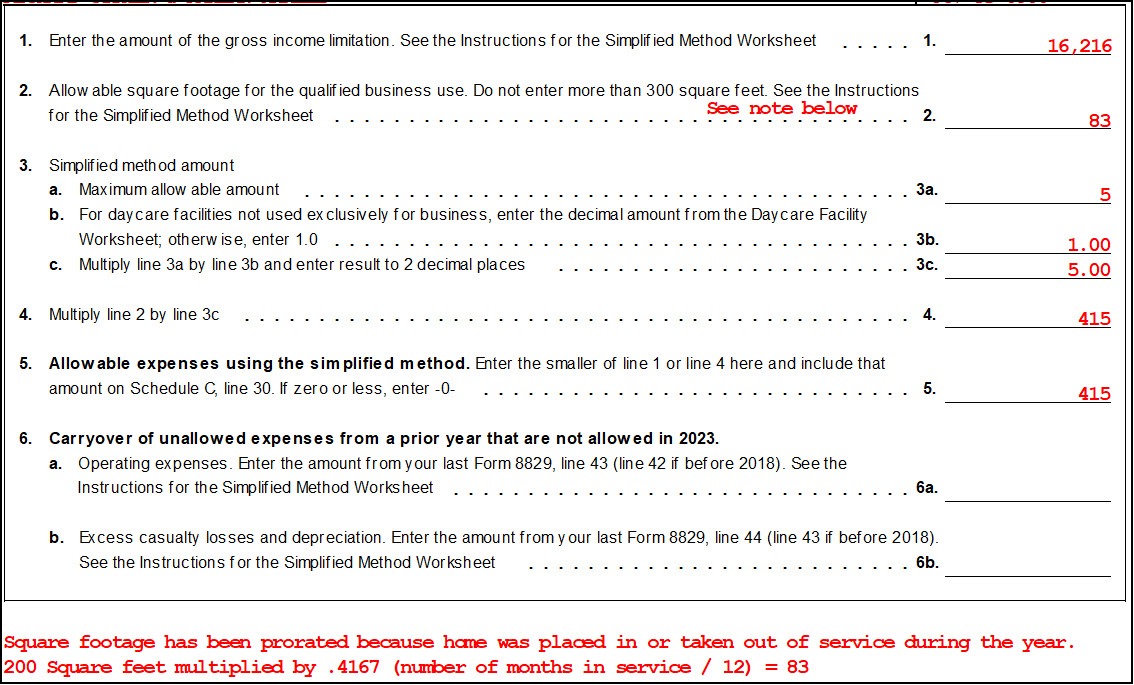

When the taxpayer elects to use the simplified method, Form 8829 is not produced; the calculated amount will flow to the applicable schedule instead. The calculation is shown Form 8829 - Simplified in View/Print mode.

- Schedule C, line 30

- Schedule E, line 19

- Schedule F, line 32

- Form 2106, line 4

- Schedule E pg2, line 28 as UPE (Unreimbursed Partnership Expenses)

- Form 4835, line 30

In the example above, Schedule C displays the calculations on line 30:

Part-year Calculation

If the office-in-home was only used for part of the year, complete the 8829 screen as above (the square footage of office on line 1, the total square footage of the home on line 2, and the checkbox Use the simplified method). Then, enter either the Date placed in service or the Date taken out of service in part III.

Note that this can only be used for one 8829 screen. Per Publication 587, "If you used more than one home in your business during the year (for example, you moved during the year), you can elect to use the simplified method for only one of the homes. You must figure the deduction for any other home using actual expenses."

In this circumstance, the total deduction still flows to the schedule and the calculation displays on the worksheet Form 8829 - Simplified. In addition, a note explaining the amount on line 2 allowable square footage includes the multiplier as a decimal (figured by number of months in service, divided by 12).

In this example, the 200 square foot amount entered on the 8829 screen is reduced to only 83 square feet allowed because the office was only used for 5 months out of the year (January-May). 300 x (5/12) = 83. This follows the guidelines from Publication 587, page 26 for part II of the Area Adjustment Worksheet.

For more information see:

On a scale of 1-5, please rate the helpfulness of this article

Optionally provide private feedback to help us improve this article...

Thank you for your feedback!