How do I enter code Intangible Drilling Costs, from box 12 of Form K-1S?

Intangible Drilling Costs can either be:

- deducted in full as a current business expense, or

- amortized over a 60 month period.

Deducting in Full as a Current Business Expense

Use screen K1S, box 12, code J4 in Drake23. In Drake22 and prior, use screen K1S, box 12, code JD. The amount carries to Form 7203, line 44 (basis worksheet Wks K1S Detail Adj Basis, line 9m in Drake20 and prior). Depending on the shareholder's participation in the S corp (active or passive), basis in the S corp, and S corp income (loss), IDC amounts may be able to offset current year income - review Form 7203 (previously Wks K1S Detail Adj Basis).

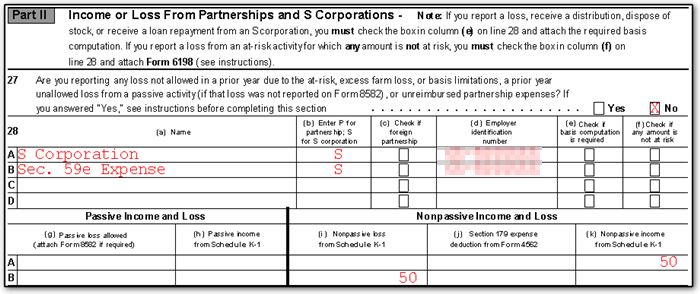

If the S corp is not a passive activity, Intangible Drilling Costs allowed will show as a loss on Schedule E, Page 2, Part II with a description of Sec. 59e Expense:

If the S corp is a passive activity, the deduction will still be calculated on Form 7203 or Wks K1S Detail Adj Basis, but the expense is not separately reported on Schedule E, page 2 as amounts carry to form 8582 first to determine any Passive Activity Loss Limitations.

Amortizing Intangible Drilling Costs

If the IDC deduction should be amortized over a five year period instead of being taken in full, the entry should be removed from the K1S screen and entered on the 4562 screen. Use the FOR and Multi-Form Code boxes to associate the 4562 with the K1S screen to which it belongs.

Note: IDC amounts may be subject to Alternative Minimum Tax as well - see Related Links below.

See Shareholder's Instructions for Schedule K-1 (1120-S) for more information.

On a scale of 1-5, please rate the helpfulness of this article

Optionally provide private feedback to help us improve this article...

Thank you for your feedback!