Choose from the following Frequently Asked Questions about Form 2210:

For what is Form 2210 used?

Form 2210 is used to calculate a penalty when the taxpayer has underpaid on their estimated taxes (quarterly ES vouchers). This penalty is different from the penalty for paying your taxes late. Form 2210 is not generated unless there is an underpayment and the form is required. See the Form 2210 Instructions for details.

Notice 2019-55 changed the 2210 waiver guidelines for 2018. Per the IR-2019-55, "The IRS is lowering to 80 percent the threshold required to qualify for this relief. Under the relief originally announced Jan. 16, the threshold was 85 percent. The usual percentage threshold is 90 percent to avoid a penalty." The software automatically calculates and applies the revised thresholds in Drake18.

The software does not calculate any interest that may be charged by the IRS on the underpayment penalty.

Where in data entry can I produce Form 2210?

By default, the software calculates the estimated tax penalty and displays it on Form 1040, line 38 (line 24 in Drake19, line 23 in Drake18, line 79 in Drake17 and prior). Form 2210 is not generated unless there is an underpayment and the form is required.

This default setting can be changed for a single return on screen 1 under 2210 Options, and the 2210 can also be forced to print by selecting the applicable code in the 2210 section on screen 1. If you select to force the 2210, but nothing produces, this is because the amount owed on the return is less than $1,000, therefore, no penalty calculates and the 2210 is not required. See Publication 505 for more information.

If you want to have the software mark the waiver option "1e" on Form 2210, "Reason for filing underpayment of estimated tax", select the most applicable check box in the upper left corner of the 2210 screen for the options in Part II, Reasons for Filing.

If the return was updated from the preceding year, unless you have entered a different amount, the field 20YY Fed tax contains the total federal tax due the preceding year (from line 16 of a 1040, for example). Similarly, the field 20YY State tax displays the equivalent tax due from the preceding year state return. Both the 20YY Fed tax and 20YY State tax fields on screen 1 will display as a green 'unverified field' if the return has been updated from the prior year. If you did not prepare the prior year return in Drake and update it to the current year, you can manually enter the prior year tax amount to have Form 2210 calculate, if needed. See Related Links below for information on clearing flagged/unverified fields.

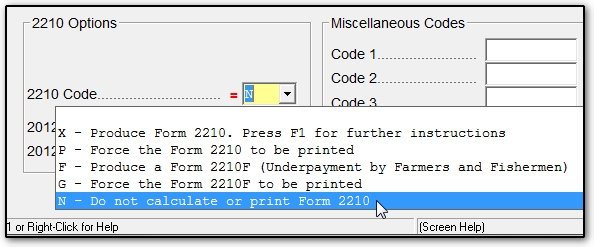

How do I suppress calculation of the underpayment penalty?

You can suppress an underpayment penalty on screen 1 in the return. Select code N from the 2210 Code drop list (bottom of the screen):

Code N will suppress Form 2210 in the event it is being produced. It will also produce note 049. You can adjust the calculation by making entries on the 2210 screen or on screen 5.

A taxpayer is in a disaster area; are penalty calculations impacted?

When calculating Form 2210, Drake Tax follows the standard guidelines without regard to disaster area declarations. If the taxpayer paid penalties for underpayment of estimated taxes, but is eligible for penalty relief under a designated disaster, they will receive a letter from the IRS showing their recalculated penalty with disaster guidelines applied. This would result in a refund of the penalty amount as allowed by the specific disaster declaration.

The IRS letter will show the dates and rates used to recompute the penalty. Review the IRS Tax Relief page for a list of all disaster tax relief by year and affected area. Each announcement will detail what relief is available, and for what time period. For more information about disaster relief, see KB 13729.

Why is a farmer's return producing a penalty on Form 2210, and it's not yet March 1st?

On the 2210 screen, you must check the Use Form 2210-F box and enter the Date Balance Paid. Penalty is avoided if the balance is paid on or before March 1st of the processing year.

On a scale of 1-5, please rate the helpfulness of this article

Optionally provide private feedback to help us improve this article...

Thank you for your feedback!