Where do I enter the net investment income tax?

Individuals, estates, and trusts may be subject to the net investment income tax (NIIT). NIIT is a 3.8% tax on the lesser of net investment income or the excess of modified adjusted gross income (MAGI) over the threshold amount.

Net investment income may include rental and royalty income, income from partnerships, S corporations and trusts, and income from other passive activities reported on your Schedule E. Taxpayers should use Form 8960 to figure this tax.

The 3.8 percent Net Investment Income Tax applies to individuals, estates and trusts that have certain investment income above certain threshold amounts. In general, investment income includes, but is not limited to: interest, dividends, capital gains, rental and royalty income, non- qualified annuities, income from businesses involved in trading of financial instruments or commodities, and businesses that are passive activities to the taxpayer.

The thresholds (based on filing status):

- $250,000 (Married Filing Joint and Qualifying Surviving Spouse)

- $125,000 (Married Filing Separately)

- $200,000 (Single or Head of household)

See the 8960 Instructions for more information.

Data Entry

The 8960 screen is located on the Taxes tab in data entry of the return. Overrides may be made on this screen, however, generally the form will be calculated when there is income subject to this tax entered elsewhere on the return.

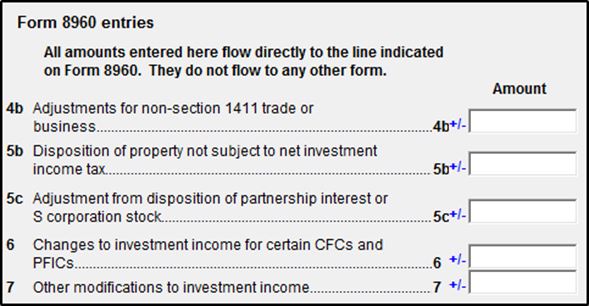

If the income from Schedules C, E, F, or Form 4835 should flow to Form 8960, check the applicable checkbox on the screen:

- C screen - Carry to 8960 line 7

- E screen - Carry to 8960 line 4b

- F screen - Carry to 8960 line 7

- 4835 screen - Carry to 8960 line 4b

The K1P, K1S, and K1F screens have specific Form 8960 entry sections, located on the 2nd page of K1 data entry (in a 1040 or 1041 return). Note that these are adjustment fields. Other data flows directly from applicable lines. The preparer should review amounts reported on the Schedule K-1 that the taxpayer received from the pass-through entity, including any amounts on:

- Partnership Schedule K-1, line 20, code Y

- S corp Schedule K-1, line 17, code U

- Fiduciary Schedule K-1, line 14, code H.

- Review the 8960 Instructions for more specific details on reporting the box 14 amount.

In view mode, worksheet Form 8960 Attachment displays the detail for specific lines.

Form 8960 can be e-filed with a taxpayer return. The Form 8960 Attachment is not transmitted and exists solely for record-keeping purposes.

If Form 8960 is not produced, check the Activity Code on the K1 screen. Non-passive activities may not be subject to this tax. Force the form to produce by using the Produce Form 8960 checkbox on the PRNT screen.

Worksheets and Common Questions

Worksheets will produce as needed based on data entry. There is no way to force the 8960 worksheets referenced below. You can force Form 8960 to print by checking the option on the PRNT screen in data entry of the relevant return.

Depending on the circumstances, rental real estate income may or may not be subject to NII tax. The software will default to carrying amounts to Form 8960, however, adjustments may be needed on screen 8960 if the real estate income (including the sale of a rental property) is exempt from NII. See the Form 8960 line instructions and the note about real estate professionals (page 3) for details.

See the instructions for details on the following guidelines on the line 9 calculation:

- Line 9a comes from Schedule A data entry, line 9, or from Form 4952, line 8 (see instructions for other limitations).

- Line 9b is calculated from the state, local, and foreign income tax attributable to NII - generally Schedule A, line 7.* This amount is subject to limitation based on the ratio of Form 8960, line 8 divided by the AGI on Form 1040.

- For example, state income tax deducted was limited to $10,000 on Wks SALT. The amount on Form 8960, line 8 is $25,000 with an AGI of $100,000. The total amount allowed to flow to Form 8960, line 9a would be (25000/100000) X 10000= $2,500.

- *Note: If state income taxes are deducted on Schedule A, line 5a and then a state issues a refund of some or all of those taxes, the refund may have to be reported as income in the following year. By default, the program will deduct sales tax instead of income tax on the Wks SALT. If you need the income taxes to flow to Form 8960, you will have to mark the Force income tax checkbox on screen A, line 5 to force the income taxes to be deducted instead of the sales taxes. Be sure to fully review the return to determine if this is more beneficial to your taxpayer.

- Line 9c - in prior years, 9c generally came from Form 4952, line 5, however, it is not allowed in 2018-2025 (8960 Instructions: "Miscellaneous itemized deductions [are] suspended for tax years 2018 through 2025. Miscellaneous itemized deductions under section 67 are not allowed for tax years beginning after 2017 and before 2026. See section 67(g).") 9c will be blank in Drake18 - Drake25.

In Drake16 and Drake17, see these Form 8960 worksheets for the calculation of lines 9 and 10:

- Wks 8960 pg 1 - worksheet for Parts I and II.

- Wks 8960 pg 2 - worksheet for Part III.

- Wks 8960 pg 3 - worksheet for Part IV.

- Form 8960 Attachment - line source details.

In Drake15, see these Form 8960 worksheets for the calculation of lines 9 and 10:

- WK896091 - worksheet for Parts I and II.

- WK896092 - worksheet for Part III.

- WK896093 - worksheet for Part IV.

- 8960_ATT - line source details.

In Drake14, the 8960_ATT provides detail about the calculation for line 9.

In Drake13, there are no worksheets available.

On a scale of 1-5, please rate the helpfulness of this article

Optionally provide private feedback to help us improve this article...

Thank you for your feedback!