How is the credit for the elderly or disabled calculated?

A non-refundable credit for those over age 65 or permanently and totally disabled is figured on Schedule R. The software figures the credit and generates the schedule, if it is applicable. Use screen R only when it is necessary to enter taxable disability income in the following scenarios:

- If it is not entered elsewhere on the return, or

- If it is for taxpayers under age 65 who are permanently and totally disabled.

- In this case, you also must indicate a physician's statement for Part II of Schedule R by selecting the appropriate option located at the bottom of screen R.

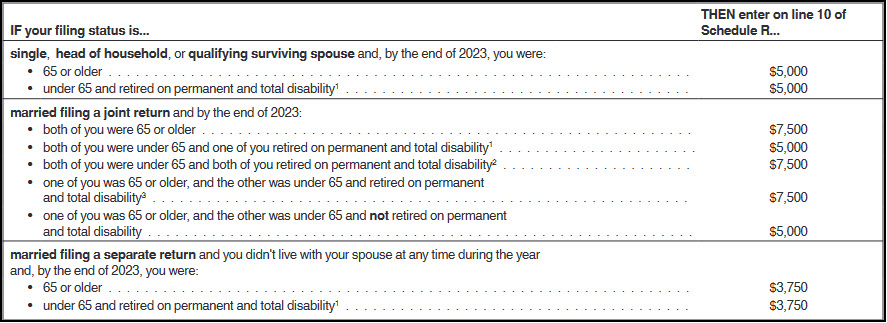

The credit is 15% of a calculated amount, which is the specified initial amount reduced by an amount based on taxpayer’s AGI and the sum of income from tax-free pensions and annuities (including income reported on 1099-R and 1099-SSA).

Initial amounts are found in Table 2, Publication 524.

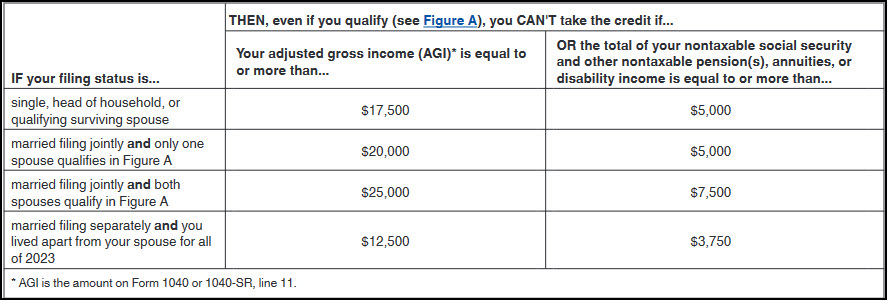

The credit is eliminated at the income levels shown in Table 1 of Publication 524:

Note 161 may produce if entries are made on screen R, but the credit is not allowed on the return. Check to ensure that they meet the requirements and that there is a tax liability against which the credit can be applied.

On a scale of 1-5, please rate the helpfulness of this article

Optionally provide private feedback to help us improve this article...

Thank you for your feedback!