What entries are needed when selling my primary residence that was also used as a rental property?

Before taking into account the rental property, you must first see if you qualify to exclude all or part of any gain

from the sale of your main home. Your main home is the one in which you

live most of the time.

Ownership and Use Tests

To claim the exclusion, you must meet the ownership and use tests.

This means that during the 5-year period ending on the date of the sale,

you must have:

- Owned the home for at least two years (the ownership test)

- Lived in the home as your main home for at least two years (the use test)

Periods of Non-qualified Use

In most cases,

gain from the sale or exchange of your main

home will not qualify for the exclusion to the extent

that the gains are allocated to periods of

non-qualified use. Non-qualified use is any period

after 2008 during which neither you nor

your spouse (or your former spouse) used the

property as a main home with the following exceptions.

Exceptions.

A period of non-qualified use

doesn’t include:

- Any portion of the 5-year period ending on

the date of the sale or exchange after the

last date you (or your spouse) use the

property as a main home;

- Any period (not to exceed an aggregate

period of 10 years) during which you (or

your spouse) are serving on qualified official

extended duty:

-

As a member of the uniformed services;

- As a member of the Foreign Service

of the United States; or

- As an employee of the intelligence

community; and

- Any other period of temporary absence

(not to exceed an aggregate period of 2

years) due to change of employment,

health conditions, or such other unforeseen

circumstances as may be specified

by the IRS.

For more information on non-qualified use, see Pub 523 page 13.

Entering the Sale of Primary Residence

To enter the sale, go to the HOME Sale of Residence screen located on the Income tab in data entry. You will enter any applicable information. Then, on line 10, enter the amount of depreciation allowed/allowable for business use. Per the IRS, even if no depreciation deduction was taken, the net profit or loss on the disposition of the property must be computed as if depreciation was actually taken. See Pub 544 for more information.

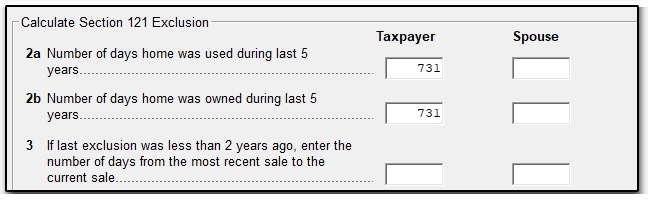

Then enter the number of days to calculate the Section 121 Exclusion.

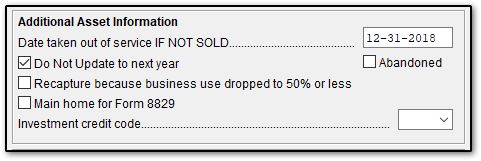

On the 4562 screen, you will enter the Date taken out of service IF NOT SOLD and check the box Do Not Update to next year. If you enter a property type, date sold, or sale price on this screen, it could double up the amount if you are reporting the sale on the HOME screen.

Property Partially Used For Business

Determine whether the space used for business during the 5 years before the sale is considered to be within your home or not. If the business or rental space was physically part of the living area of your home, such as a spare room used as a bed-and-breakfast bedroom or attic space used as a home office, your business usage doesn’t affect your gain/loss calculations.

Determine whether the business or rental space still counts as a business space. A space formerly used for business is considered residence space if ALL of the following are true:

- You weren’t using the space for business or rental at the time you sold the property,

- You didn’t earn any business or rental income from the space in the year you sold your home, and

- You used the space as residence space for 2 years out of the 5 years leading up to the sale.

If all of these are true, your business usage DOESN’T affect your gain/loss calculations.

In certain situations, the sale of the property must be treated as the sale of two separate properties. For example, the property sold is a farm, and the farmhouse meets both the ownership test and the use test, but the barn does not meet the use test. In this case, the selling price, selling expenses, basis, and the allowable Section 121 exclusion must be apportioned between the home itself and the business or rental portion.

Starting in Drake18, use the section Business or Rental Use of Home to enter the percentage of the property used for the business or rental. See the field help (F1) for details. When an entry is made in that field, Wks Home is produced in view mode that shows the allocation of the gain and/or loss for personal and business use. The business portion is then carried to Form 4797 and/or Schedule D. The personal portion is carried to Wks 2119 to determine the taxable amount, if any.

Important: Review the worksheets in view mode for accuracy-- in some circumstances, an entry may still be required on the 4797 screen to allocate the business income (loss).

In Drake17 and prior, enter the portion of all amounts that pertain to the main home on the HOME screen and make a separate entry on the 4797 screen for the business component.

Additional selections on the HOME screen may be needed in certain circumstances:

See Publication 523 for more information.

On a scale of 1-5, please rate the helpfulness of this article

Optionally provide private feedback to help us improve this article...

Thank you for your feedback!