How do I get the recovery rebate credit to be calculated on Form 1040, line 30?

Due to COVID-19, most eligible taxpayers received economic impact payments during 2020. The first EIP was issued in summer 2020 and the second was scheduled to be issued between December 2020 and January 2021. To ensure that all eligible taxpayers received the proper amount, an entry must be made* on the 2020 tax return to reconcile the EIP amounts received with the amounts for which the taxpayer is eligible. If the taxpayer received a lower amount for the payments (or did not receive the stimulus payments at all), they may be eligible to claim the recovery rebate credit on their 2020 tax return.

Note: If a taxpayer is eligible for the Recovery Rebate Credit, but does not have anything else to report on a return, they can file a 2020 return to claim the credit. There would not be another way to file and claim EIP1 or EIP2, if not previously received. Since the RRC is a refundable credit, eligible taxpayers can e-file their 2020 return to claim the Recovery Rebate Credit, even if they had zero income in 2020, but are otherwise eligible.

The first EIP was issued in the following amounts: $1200 per taxpayer ($2400 for joint filers) and $500 for each qualifying child. The second EIP was issued in the following amounts: $600 per taxpayer ($1200 for joint filers) and $600 for each qualifying child.

For the first EIP, Notice 1444 was issued to taxpayers reporting the amount of EIP received. Notice 1444-B will be issued to report the amount of EIP received in the second payment. Enter those amounts on the RRC screen in the following boxes:

- Enter the first payment in the box Enter the amount, if any, of the economic stimulus payment you received (before offset). This was generally received in Summer 2020. This amount can be found on Notice 1444.

- Enter the second payment in the box Enter the amount, if any, of the second economic stimulus payment the taxpayer received (before offset). This was generally received between late December 2020 and mid-February 2021. This amount can be found on Notice 1444-B.

If the taxpayer did not receive one or both of the economic stimulus payments, enter a zero (0) in the applicable box(es).

In view mode, Wks Recovery Rebate calculates whether the taxpayer is eligible for an additional credit on Form 1040, line 30.

Common Scenarios and Troubleshooting

Choose from the following topics for more information:

Qualifying Child

If you are expecting an additional credit to be calculated, review the requirements for a qualifying child for the EIP or Recovery Rebate Credit:

"You will receive an additional $500 Payment1 for each qualifying child you claimed on your tax return being used to calculate your Payment. Here's the criteria you should consider:

- Relationship to the individual who is eligible for the Payment: The child is the son, daughter, stepchild, eligible foster child, brother, sister, stepbrother, stepsister, half-brother, half-sister, or a descendant of any of them (for example, grandchild, niece, or nephew).

- Child's age: The child was under age 17 at the end of [2020]2

- Dependent of the individual who's eligible for the Payment: The child is claimed as a dependent on the 2018 or 2019 tax return or entered on the Non-Filers: Enter Payment Info Here tool.

- Child's citizenship: The child is a U.S. citizen, U.S. national, or U.S. resident alien.

- Child's Residency: Child must have lived with the individual eligible for the Payment for more than half the tax year.

- Support for Child: Child must not provide over half of own support for the tax year.

- Child's taxpayer identification number: The child has a valid work eligible Social Security number or an Adoption Taxpayer Identification Number (ATIN) that was issued before July 15, 2020."

1$500 applies to the first EIP issued. The second EIP allows for $600 per qualifying child. The guidelines for a qualifying child are the same for both payments, with the exception of the tax year. EIP was based on the 2019 return; the RRC is based on the facts of the 2020 return.

2The IRS FAQs say the end of the taxable year and mention 2019 with regards to the EIP. The taxable year for the purposes of the Recovery Rebate Credit is 2020, so the child would have to have been under the age of 17 as of December 31, 2020 to be a qualifying child. Review the worksheet in page 59 of the 1040 Instructions for details.

Note that the credit is based on the total persons eligible to be claimed in 2020. For example, a couple filing MFJ has two children. Child A turned 17 in 2020 and Child B was born in 2020. Since the guidelines require an eligible child to be under the age of 17, Child A is no longer a qualifying child. Child B is a qualifying child in 2020. The total number of eligible children for the purposes of RRC, however, on the 2020 return is only 1. If they already received the EIP 1 in the amount of $2900 (2 adults + 1 dependent) and EIP 2 of $1800 (2 adults + 1 dependent), no additional amount is calculated or due.

Separated or Divorced Parents

Some separation/divorce agreements allow dependents to be claimed on each parent's return in alternating years. The EIP payments were based on which taxpayer claimed that dependent on the 2018/2019 return. The RRC is based on which parent claims the dependent on the 2020 return. Thus, if parent A claimed the dependent in 2018/2019, they would have received EIP payments for that dependent. Then, if parent B is claiming the dependent in 2020, they may be eligible for the RRC for that dependent. There is no provision requiring the EIP to be repaid. Per the IRS Frequently Asked Questions:

"No, there is no provision in the law that would require individuals who qualify for a Payment based on their 2018 or 2019 tax returns, to pay back all or part of the payment, if based on the information reported on their 2020 tax returns, they no longer qualify for that amount or would qualify for a lesser amount.

...

For example, you received $500 for your child whom you claimed on your 2018 or 2019 tax return. You do not claim the child on your 2020 tax return because the child’s other parent claims the child. You will not be required to pay back the $500 even if the child’s other parent claims $500 for the same child on his or her 2020 tax return."

The preparer should review the return to determine if the taxpayer meets all eligibility requirements (listed above).

Former Dependents

If the taxpayer was claimed as a dependent on a 2019 return, but is not a dependent of another in 2020, they may be eligible for the RRC even if the person who claimed them on the tax year 2019 return received the stimulus payment(s) for them in calendar year 2020. The Recovery Rebate Credit is based on the facts of the 2020 tax return. If they meet all the requirements, the software will calculate the credit. If you determine that they should not receive the credit, or the taxpayer does not want to claim the credit, check the box Taxpayer is not claiming any Recovery Rebate Credit at the bottom of the RRC screen.

MFJ to MFS

If the 2019 return was filed as MFJ and they are filing their 2020 return as MFS, the amount of EIP 1 and EIP 2 shall be split in half per the 1040 Instructions:

"If your EIP 1 or EIP 2 was based

on a joint return, you and your spouse

are each treated as having received half

the payment that was issued."

If using the split return process, 1/2 of the amount entered on the RRC screen will be carried to the RRC screen in the MFS return, without regard to the TSJ box on the dependent screen (if present).

SSN Requirement

The Consolidated Appropriations Act, 2021 repealed the requirement for both taxpayers to have a valid SSN for any EIP to be allowed. This guideline applies retroactively to the first EIP as well as the second. This is also used when calculating the Recovery Rebate Credit. As long as either the taxpayer or the spouse has a valid SSN, the EIP or credit is allowed for the SSN taxpayer and any dependent children that also have a valid SSN. The spouse with the ITIN is not eligible to receive the RRC (or EIP) unless the taxpayer was a member of the Armed Forces during 2020. No amount of credit or EIP is allowed for dependent children that do not possess a valid SSN. The software will calculate the RRC based on the eligible individuals entered on the return as well as the EIP amounts entered on the RRC screen.

A valid SSN is defined as "...one that is valid for employment in the United States and is issued by the Social Security Administration (SSA) before the due date of [the] 20YY tax return..." If none of the taxpayers on the return possess valid SSNs, you can suppress the calculation of the RRC for the individual who does not have a valid SSN by checking the applicable box at the bottom of the RRC screen or screen 2 (if a dependent):

- Taxpayer's SSN is not valid for Employment at the bottom of the RRC screen.

- Spouse's SSN is not valid for Employment at the bottom of the RRC screen.

- Don't include in RRC calc at the bottom of screen 2 for the relevant dependent(s).

The option at the bottom of the RRC screen Taxpayer is not claiming any Recovery Rebate Credit will suppress the entire RRC calculation on the return.

Deceased Taxpayer

If the taxpayer died in 2020, meets the other requirements, but did not receive the full amount of EIP1 and/or EIP2, they are eligible for the Recovery Rebate Credit on their 2020 tax return. Per the 1040 Instructions:

"Generally, you are eligible to claim the recovery rebate credit if in 2020 you were a U.S. citizen or U.S. resident alien, weren't a dependent of another taxpayer, and have a valid social security number. This includes someone who

died in 2020, if you are preparing a return for that person."

Suppressing Calculation

If the taxpayer does not want to claim the credit, check the box Taxpayer is not claiming any Recovery Rebate Credit at the bottom of the RRC screen. This will suppress the entire RRC calculation for the return. If the taxpayer/spouse/dependent does not have a valid SSN, see above for suppressing the calculation for that individual.

Note: you still have to enter the amount of stimulus payments received (even if zero) on the RRC screen to prevent the EF message regarding missing required data.

Phase-out Limitations

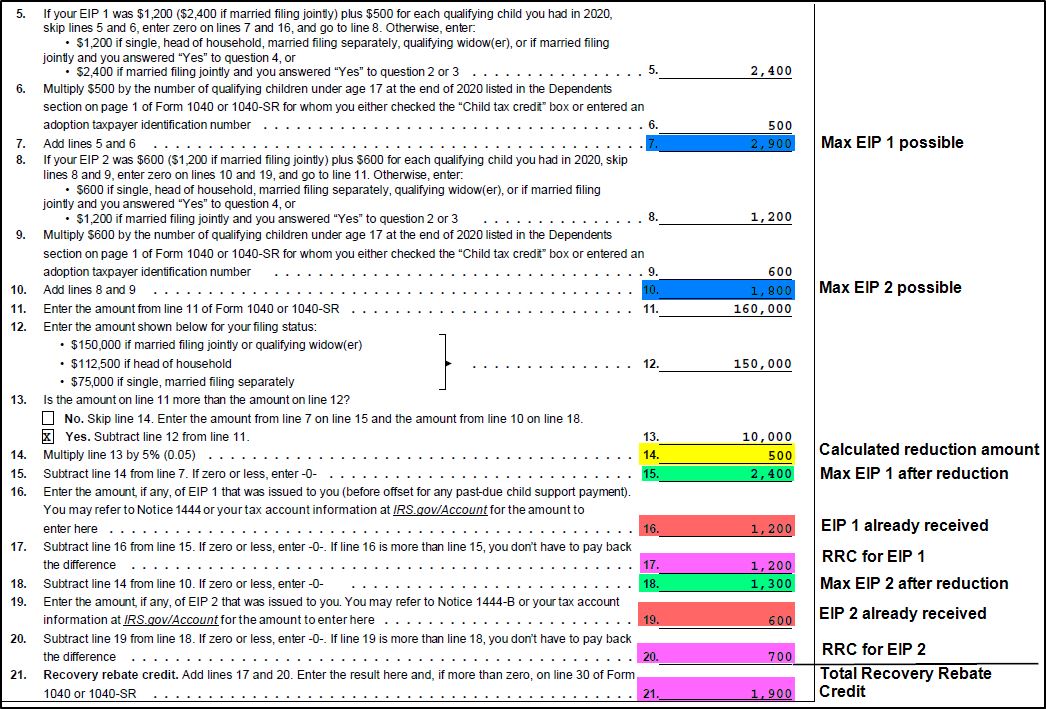

The RRC is subject to limitations. Per the IRS: "Your recovery rebate amount will be phased out if your adjusted gross income for 2020 exceeds $150,000 if you are married filing a joint return, $112,500 if you are using the head of household filing status, or $75,000 if you are using any other filing status." The IRS goes on to discuss the reduction: stating that: "An individual’s payment is reduced by 5% of the excess of the individual’s AGI over the applicable threshold." In addition, "For individuals with qualifying children, these total-phaseout amounts increase by $10,000 for each qualifying child. For example, for an eligible individual filing as married filing separately with 3 qualifying children, the individual’s payment is reduced to $0 if his or her AGI is $129,000 or more." The credit will be reduced to $0 once AGI reaches and exceeds $198,000 for joint filers, $136,500 for a head of household, and $99,000 for everyone else.

When applicable, the Wks Recovery Rebate will calculate the reduction amount required based on the filing status and adjusted gross income (AGI). This is shown on line 14 of Wks Recovery Rebate. This reduction amount is subtracted from both EIP 1 and EIP 2, if present. Below is an example of the worksheet for a MFJ return with one qualifying child that received less than the full amount of EIP 1 and EIP 2:

*If the income on the return is over the applicable phase-out threshold, no entry is required on the RRC screen.

Taxpayer Notices

Taxpayers may receive notices regarding the recovery rebate credit and any changes that were made by the IRS. The following table summarizes some of the CP codes and their meanings.

| 681 |

We changed the amount claimed as a Recovery Rebate Credit on your tax return. Information on your return indicates that either you (or your spouse if married filing jointly) is claimed as a dependent on another taxpayer's tax return. |

| 682 |

We changed the amount claimed as Recovery Rebate Credit on your tax return. The error was in one or more of the following:

- Your Social Security number (or your spouse's Social Security Number if married filing jointly) was either missing or incomplete.

- Your last name (or your spouse's last name if married filing jointly) does not match our records.

- You (or your spouse if married filing jointly) used an Individual Taxpayer Identification Number (ITIN) and there is no indication that one spouse was a member of the Armed Forces of the United States at any time during the tax year, so that an exception does not apply to the rule that both spouses must have a Social Security number.

- We compared the Social Security numbers (SSN) shown on your tax return with records from the Social Security Administration. According to these records, the SSN shown on your tax return for you, your spouse, or one or more of the dependents belongs to a deceased person. You must contact the Social Security Administration if this information is incorrect.

- The Social Security number shown on your tax return for you, your spouse, or one or more of the dependents listed on your return was not issued before the due date of the tax return.

|

| 683 |

We changed the amount claimed as Recovery Rebate Credit on your tax return. The error was in one or more of the following:

- The Social Security number of one or more individuals claimed as a qualifying dependent was missing or incomplete.

- The last name of one or more individuals claimed as a qualifying dependent does not match our records.

- One or more individuals claimed as a qualifying dependent exceeds the age limit.

- Your adjusted gross income exceeds $75,000 ($150,000 if married filing jointly, $112,500 if head of household).

- The amount was computed incorrectly.

|

For more information about IRS adjustment letters citing the RRC, see the Newswire IR-2021-76 and the IRS RRC Topic G page.

For more information about the recovery rebate credit, see the IRS instructions, Topic J, and Notice 1444. For a demonstration, watch the video Recovery Rebate Credit.

For details about the new Advance Child Tax Credit Payments in 2021, see the IRS website.