How do I deduct employee business expenses on Form 2106?

Starting in Drake18, the Tax Cuts and Jobs Act suspends all miscellaneous itemized deductions that are subject to the 2% of adjusted gross income floor. This change affects un-reimbursed employee expenses such as uniforms, union dues and the deduction for business-related meals, entertainment and travel. Please review Notice 2018-42 for more information.

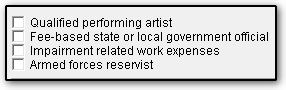

Taxpayers whose un-reimbursed expenses would flow to Schedule 1 line 24 such as performing artists (QPA), armed forces reservists, fee-based state or local government officials, and disabled employee with impairment-related work expenses are still able to take this deduction. At the top of screen 2106 is a checkbox to make this indication. Some states may not conform to this change and could require this screen to be completed for state purposes only, even if the taxpayer cannot deduct expenses for federal purposes.

Note: If screen 2106 is completed for a member of the clergy in Drake18, select Pastor – Carry 2106 amount to CLGY worksheet to carry the 2106 to the Clergy worksheet to offset self-employment income.

Certain taxpayers may take mileage (which includes a factor for depreciation) or actual expenses (such as oil and gas) along with depreciation. Taxpayers may not take both mileage and depreciation since the mileage calculation includes depreciation.

Meals/entertainment expenses are only allowed at 50% except for taxpayers subject to DOT rules, in which case they are allowed 80% for meals. If the taxpayer is subject to DOT rules, enter the total meals/entertainment expense in the first field on Line 5b of the 2106 screen and in the second field enter the amount of that expense that is attributable to DOT hours of service rules for meals (for example, 5000 was spent and 4000 was subject to DOT rules).

In Drake17 and prior:

- The result of Form 2106 flows to Schedule A, line 21, not to the 1040 directly unless a checkbox in the bottom-right is marked to direct the deduction to Form 1040, line 24 (2017).

- If the taxpayer is a member of the clergy, select Pastor – Carry 2106 amount to CLGY worksheet to carry the 2106 to the Clergy worksheet and the Schedule A, line 21 as applicable.

Note: If there are two vehicles on the 2106 screen, the software will generate the Form 2106 long form with information for both vehicles automatically. There is not a way to force the Form 2106-EZ if there is more than one vehicle on the form. Form 2106-EZ is not available starting in Drake18.

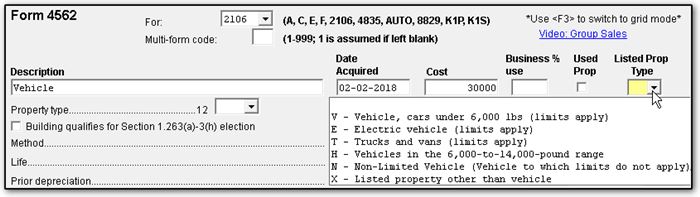

How do I get information to flow to Section D (Depreciation of Vehicles) of the 2106 from 4562 data entry?

Section D of Form 2106 reports the depreciation of vehicles. To move an asset to Section D select V, E, T, H, or N as the Listed Property Type on the 4562 screen for that asset.

When screen 4562 is directed to flow to Form 2106:

- Form 4562 is not needed and does not generate.

- If mileage is used on Form 2106, it already includes a depreciation component.

- If actual expenses are more favorable to the taxpayer than mileage or if actual expenses are forced on screen 2106, depreciation from screen 4562 is reported on Form 2106, even though Form 4562 is not produced in View.

How do I get amounts to carry from screen 8829 to Form 2106?

Go to the 2106 screen in data entry. Make sure it has either a T or S code entered. Beginning in 2018, you will also need to indicate one of the following, if applicable:

- Qualified performing artist

- Fee-based state or local government official

- Impairment related work expenses

- Armed forces reservist

Next, go to the 8829 screen in data entry. Enter 2106 in the FOR field and enter the appropriate code in the multi-form code field.

How do I clear EF message 5132?

INCOME EXCEEDS LIMIT: Business expenses for a qualified performing artist, entered on screen 2106, are permitted only when the taxpayer's AGI is $16,000 or less before deducting any expenses as a performing artist.

Per IRS instruction, in order for a performing artist to qualify to take a 2106 deduction, the taxpayers AGI must be below $16,000 before 2106 expenses are taken into consideration.

Additional Resources:

How do I clear EF message 5183 when the same taxpayer has more than two 2106 Forms?

Starting with Drake14, if the same individual on a return has more than two 2106 forms, EF message 5183 will generate:

There is a limit of two Form 2106 per taxpayer (plus two per spouse, if appropriate) to be eligible for e-file.

To report more than two Forms 2106 per taxpayer (or spouse), the return must be paper-filed.

You cannot e-file a return containing more than two 2106 forms for the same individual. Such returns must be paper filed.

On a scale of 1-5, please rate the helpfulness of this article

Optionally provide private feedback to help us improve this article...

Thank you for your feedback!